LVMH tried to kill the Tiffany deal. Then closed it for $425 million less.

Inside the biggest legal dispute in luxury history and the $425M lesson at the end.

Hello, and welcome back to Buyout Diary.

If you have been reading Buyout Diary for a while, you will know that this series started with BVLGARI. Part 1 was the search, the courtship, and the deal structure. Part 2 was the integration: how Arnault absorbed a 127-year-old Italian family business without destroying what made it worth acquiring.

Part 3 is different in tone. BVLGARI was a patient story. Arnault spent years building a relationship with the Bulgari family before a single term sheet was discussed. The deal reflected that patience. The integration reflected it even more clearly.

Tiffany is not a patient story. It is a story about leverage, timing, legal brinkmanship, and what happens when a black swan event lands in the middle of the world’s largest luxury deal. It is also, ultimately, a story about the same thing BVLGARI was: an acquirer who understood what he was buying well enough to hold his nerve when everyone else was convinced the deal was dead.

We start, as always, with the question beneath the question. Not how Arnault acquired Tiffany. But why. And whether the same logic that drove the search also drove the renegotiation that followed.

1. The Symbolic Deal

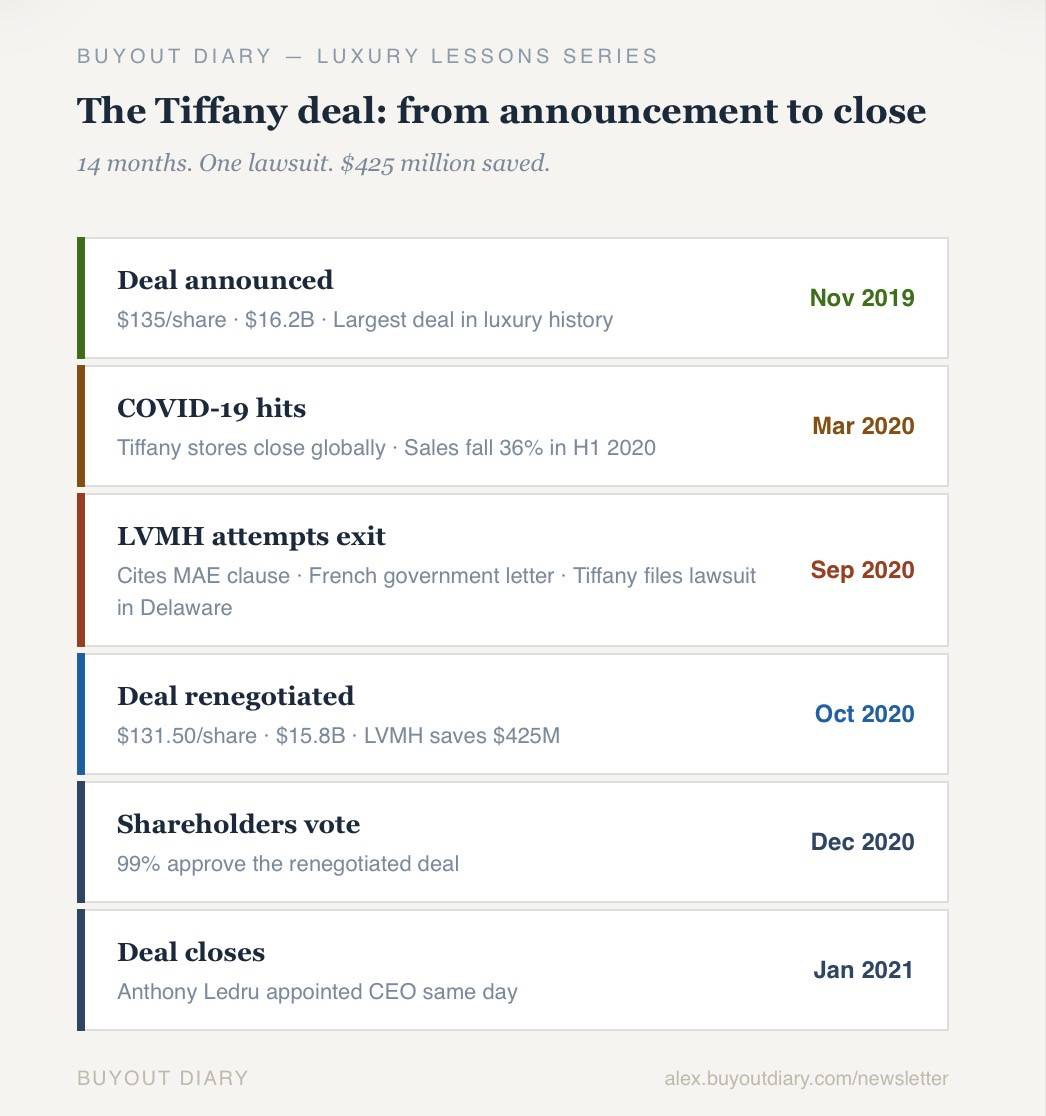

On 25 November 2019, LVMH and Tiffany announced that the French luxury group would acquire the American jeweller at $135 per share in cash, valuing Tiffany’s equity at approximately $16.2 billion (€14.7 billion at the time). It was the largest acquisition in luxury history.

The announcement language was careful and deliberate. Arnault said he had “an immense respect and admiration for Tiffany” and intended to “develop this jewel with the same dedication and commitment” applied to each of LVMH’s other maisons. Tiffany’s CEO Alessandro Bogliolo said the deal would allow the brand to “reach new heights.” Both statements were true. But neither quite captured what Arnault was actually doing.

Tiffany was not just a business with strong cash flows and a recognisable product. It was the only truly global luxury jewellery brand originating in the United States, founded in downtown Manhattan in 1837, named in films, embedded in American cultural mythology in a way that no French or Italian house could replicate. Audrey Hepburn had pressed her face against its window. American presidents had proposed with its diamonds. The blue box was recognised worldwide without any explanation.

For LVMH, acquiring that mythology was the point. Not just the revenue, not just the margins, not just the distribution network. The cultural position Tiffany held in the United States was something that could not be built from scratch, regardless of capital committed. It could only be acquired.

Arnault knew that. He had known it for years before November 2019.

2. The Strategic Fit

To understand why Arnault wanted Tiffany, you have to understand where LVMH stood in late 2019.

The group was the undisputed leader of the global luxury industry. Fashion and leather goods, Louis Vuitton, Dior, Fendi, Celine, accounted for the largest share of revenue and profit. Wines and spirits, perfumes and cosmetics, selective retailing were all profitable and growing. But one division consistently underperformed relative to its potential: Watches and Jewellery.

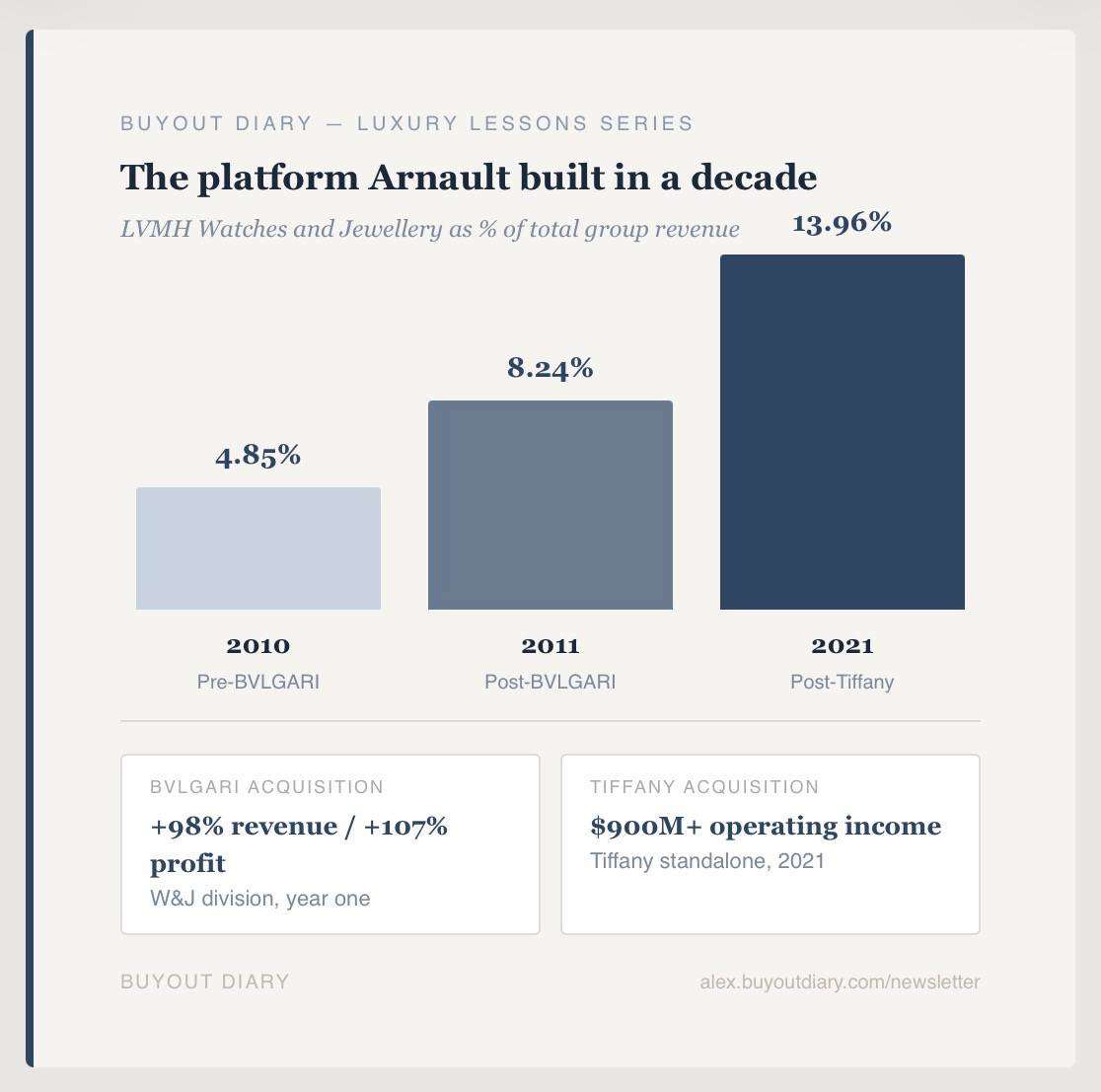

According to LVMH’s 2018 financial accounts, the Watches and Jewellery division generated €4.1 billion in revenue, just 9% of the group’s total €46.8 billion. In the first three quarters of 2019, it was growing at 8% year on year, the slowest division in the group. BVLGARI had transformed the division after 2011, pushing its share from 4.85% to over 8% of group revenue. But the division remained structurally undersized relative to LVMH’s ambitions for the jewellery category.

The second gap was geographic. Less than a quarter of LVMH’s revenue in 2018 came from the United States, a remarkable underrepresentation given that the US was the single largest luxury consumer market in the world, home to 18.6 million millionaires. Tiffany, with more than 300 stores globally and a customer base that skewed heavily American, was the most efficient way to close that gap.

The third gap was cultural. LVMH’s jewellery portfolio was built on European heritage: Roman BVLGARI, French Chaumet. There was nothing American in the jewellery category. In a market where authenticity of origin matters to consumers, that absence was a genuine limitation.

Tiffany closed all three gaps simultaneously. It was the right business at the right moment. Arnault had been watching it long enough to know when to move.

The ETA parallel: Platform thinking means asking not just whether a business is good, but whether it makes your next acquisition better. BVLGARI gave LVMH the infrastructure, the credibility, and the operational model for large-scale jewellery integration. Tiffany, built on top of that, became the American anchor to BVLGARI’s European and Asian one. Each acquisition should compound the value of the one that preceded it. That is a different question from “is this a good deal?” and it is the more important one.

3. Due Diligence and Valuation

Tiffany was not a distressed asset when LVMH approached it. But it was an underperforming one.

In the years before the acquisition, Tiffany had accumulated a specific set of challenges that individually were manageable but collectively told a story of a brand that had stopped compounding.

Revenue had been essentially flat for several years. In fiscal year 2019, Tiffany reported net sales of approximately $4.4 billion, roughly where they had been in 2015. For a brand with global recognition and 300 stores, that stagnation was striking. Arnault said so plainly after closing: “Tiffany stagnated. Both profit and revenue were flat.”

The product problem was structural. Tiffany’s range was anchored heavily towards silver jewellery at accessible price points: the sterling silver bracelet, the heart pendant, the return to Tiffany key. These were aspirational entry products that had built enormous brand recognition. But they were increasingly associated with an older customer base and a gift category, not with the high-jewellery desire that drives the most valuable luxury purchasing. The direction the category was moving, towards higher price points, statement pieces, and branded fine jewellery, was not the direction Tiffany was positioned to capture.

The geographic gap was equally clear. LVMH had spent years systematically building its presence in Asia, the fastest-growing market for luxury goods globally. Tiffany had strong brand recognition in Asia, the blue box was recognised as widely there as anywhere, but its physical retail presence and operational infrastructure in the region were not calibrated to that potential. The brand was pulling less revenue from Asian consumers than its recognition suggested was possible.

Online was the third weakness. Luxury e-commerce had been accelerating globally, and Tiffany’s digital sales channels were underdeveloped relative to what was required to serve a customer base that increasingly began its discovery and purchase journey online.

None of these were fatal. They were correctable. And the word correctable is doing significant work in Arnault’s valuation logic.

The $135 per share offer represented a meaningful premium to where Tiffany had been trading. The implied enterprise value multiple was rich by conventional financial analysis standards. But Arnault was not paying for Tiffany’s current earnings. He was applying a framework he had already proved with BVLGARI: identify a genuinely excellent brand that is temporarily underperforming due to correctable operational and strategic weaknesses, pay a premium that reflects the brand’s intrinsic position rather than its current financial results, apply capital and operational expertise, and allow the compounding to begin.

BVLGARI’s net revenue had been declining from €1.091 billion in 2007 to €890.5 million in 2010 when Arnault moved. He paid a 61% premium. Within twelve months, LVMH’s Watches and Jewellery division recorded a 98% revenue increase and a 107% profit increase. The premium looked extraordinary at announcement. It looked like a bargain within a year.

The Tiffany thesis was built on the same logic at larger scale. The brand deserved a higher price than its current earnings justified, because the gap between what it currently was and what it could become under LVMH’s stewardship was precisely the value being purchased. The premium was not irrational optimism. It was a specific calculation about what the correction of known, manageable weaknesses would produce.

He had been right about BVLGARI. He had every reason to believe he would be right about Tiffany.

The ETA parallel: The distinction between buying a distressed asset and buying an underperforming excellent business is one of the most important in acquisition strategy. Distressed assets require operational rescue. Underperforming excellent businesses require capital and the right stewardship. They are different investments with different risk profiles. Arnault has built his entire career on the second category. For self-funded buyers looking at succession businesses, the same lens applies. A business generating flat revenue for three years under an ageing owner who has not invested in it is not necessarily broken. It may be an excellent operation that has simply not had the resource or the energy to reach the next level. That gap between current state and potential is where the valuation argument lives.

4. The Negotiation War

The deal was announced in November 2019. It was supposed to close in mid-2020.

Then COVID-19 arrived.

In the first half of 2020, Tiffany was forced to close stores globally. Sales fell approximately 36%. The luxury market had entered a period of genuine uncertainty about when and how it would recover. LVMH, watching the situation develop, began to explore whether the conditions it was acquiring Tiffany under were still the conditions it had agreed to.

On 9 September 2020, LVMH made its move. The group announced that it could not close the deal by the contractual deadline of 24 November 2020, citing three reasons: first, that a Material Adverse Effect had occurred in Tiffany’s business; second, that Tiffany had not operated its business in the “ordinary course” required by the merger agreement; and third, that a letter from a French government minister had asked LVMH to delay the acquisition, linked to a trade dispute between France and the United States over a digital services tax.

Tiffany filed a lawsuit in the Delaware Chancery Court that same day, seeking a court order requiring LVMH to close on the agreed terms.

What followed was six weeks of public brinkmanship, private renegotiation, and legal preparation that never quite reached trial.

The legal position was delicate for both sides. The Material Adverse Effect clause in the merger agreement did not explicitly include pandemics or public health crises, a common omission in pre-COVID deal documentation. This was LVMH’s critical vulnerability. The pandemic had disrupted Tiffany’s business, but the legal threshold for a qualifying MAE required comparative harm rather than sector-wide disruption. Tiffany’s relative stability, compared to broader luxury market peers, made it difficult to argue that a qualifying event had occurred.

LVMH knew this. So did Tiffany. The Delaware courts are well-versed in MAE disputes and had consistently set a high bar for finding that one had occurred. LVMH’s legal arguments were defensible but not certain to prevail.

The French government letter was procedurally clever but substantively thin. A letter from a minister asking a private company to delay a commercial transaction, in the context of a bilateral trade dispute, was not a legally binding instruction. Its value lay in creating uncertainty and buying time, not in providing a robust contractual defence.

On 28 October 2020, the two sides settled. LVMH agreed to pay $131.50 per share, down from $135. The total deal value dropped to $15.8 billion, a saving of approximately $425 million for Arnault. In exchange, LVMH dropped its attempts to exit. Tiffany gained two new protections: if LVMH attempted to exit the deal again, the price would revert to $135 per share; and the French government letter clause was removed from the agreement entirely.

On 30 December 2020, more than 99% of Tiffany’s shareholders voted to approve the renegotiated deal. On 7 January 2021, it closed.

The ETA parallel: Arnault’s apparent walk-away was not a genuine attempt to exit. This is the most instructive thing about the entire episode. LVMH wanted Tiffany. The strategic logic had not changed. The pandemic had not made Tiffany a worse business than the one Arnault had assessed. It had made it a temporarily distressed one. What Arnault did was use a period of genuine external uncertainty to create legitimate grounds for renegotiation, extract a material price reduction, and close the deal he had always intended to close.

The lesson is not “threaten to walk away when the deal is under pressure.” The lesson is more precise: the buyer who understands the deal better than anyone else in the room can hold their nerve when circumstances create apparent instability. Panic is expensive. Patience and legal clarity are not.

5. Closing and Strategic Positioning

With Tiffany now formally part of the group, LVMH’s Watches and Jewellery division was transformed.

Where BVLGARI had lifted the division’s share of group revenue from 4.85% to 8.24% in a single year, Tiffany made it the fastest-growing and most visible division in the group almost immediately. By 2021, the Watches and Jewellery division accounted for 13.96% of LVMH’s total group revenue having grown from a footnote to a genuine strategic pillar in a decade.

The platform Arnault had been building since 2011 was now complete in its fundamental architecture. BVLGARI anchored the European and Asian jewellery strategy with Italian heritage and artisan manufacturing. Tiffany anchored the American market with its unmatched US brand recognition and distribution network. The two brands serve different customers, in overlapping geographies, without directly competing.

That is not an accident. It is the logic of strategic portfolio construction applied to one category. Each acquisition was designed to complement the one that preceded it, not duplicate it.

6. Five Lessons for Every Acquisition Buyer

Tiffany is a different story from BVLGARI, and its lessons are sharper. They are more uncomfortable and more directly applicable to the deals most buyers are working on at a fraction of this scale.

Strategic search is not opportunistic search. Arnault did not approach Tiffany because it was available. He approached it when its combination of brand position, geographic fit, and temporary underperformance made it the right acquisition at the right price. Knowing the difference between a business that is available and a business that deserves to be acquired is the foundation of a good search.

Platform thinking multiplies returns. Tiffany is more valuable inside LVMH than it was as a standalone business, not because LVMH is a better manager of assets, but because Tiffany completes a category architecture that BVLGARI began. Each acquisition in a portfolio should ask the same question: does this make the whole worth more than the sum of its parts?

Market timing is a legitimate lever. COVID was not just a crisis. For Arnault, it was a renegotiation opportunity worth $425 million. The buyer who understands when external conditions create a genuine basis for repricing, without acting in bad faith, has a tool that most buyers either ignore or misuse.

Sometimes walking away increases your power. LVMH’s apparent exit attempt gave Arnault something he did not have before: proof that he was willing to consider not closing. Whether or not he would have followed through, the credibility of the threat shifted the negotiating dynamic enough to extract a material concession. In any negotiation, the party who needs the deal more will pay for it.

Narrative and reputation matter in every negotiation. At no point did LVMH publicly say “we want a discount.” The public statements were always framed around legal grounds, contractual obligations, and regulatory conditions. The outcome was financial, but the language was professional. In small business acquisitions, the same principle applies. The buyer who negotiates in a way that the seller can respect will close deals that the buyer who negotiates aggressively will not.

Coming Up in the Series

The deal is closed. The legal dispute is settled. Bernard Arnault has his American jewellery anchor.

Now comes the part that tests whether the BVLGARI playbook travels across the Atlantic.

BVLGARI kept its CEO for three years. Tiffany’s CEO was replaced on the same day the deal closed. BVLGARI preserved its Roman identity with minimal external intervention. Tiffany’s brand was actively repositioned, more aggressively than anything LVMH had attempted before. BVLGARI produced record results almost immediately. Tiffany produced record results in 2021 and 2022, then began to show the limits of the playbook in 2023 and 2024.

Part 4, Tiffany & Co.: Reinventing an Icon, is the honest version of what happens when the greatest acquirer in the world meets a brand that requires something his model was not quite built for.

That issue will appear in Buyout Diary in the coming weeks.

Hit reply and tell me: what feels harder about deals to you right now, finding the right business to approach or holding your nerve through the negotiation once you have found it?

See you next Monday.

Alexander