Ten months in, my thesis has changed. Here is what moved.

Four dimensions that shifted. Two that did not. And a method to audit yours this weekend.

Hello, and welcome back to Buyout Diary.

A reflective issue this week.

Last October I wrote a Buyout Diary piece on how to build your investment thesis at the start of a search. It is still a piece I stand behind. But the thesis I wrote for myself in August 2025 is not the thesis I hold today.

Most searchers feel guilty about this. They wrote a thesis, they spent time refining it, they put it in a PPM, and now reality is pushing back on parts of it. Their instinct is to defend the original, because defending it is what a disciplined searcher does.

I do not think that is right. A thesis is a hypothesis. Hypotheses are tested by contact with reality. If yours has not moved in ten months, you have not really been searching, you have been performing a search against a document you refuse to update.

This issue is the honest update. Four dimensions of my own thesis that have shifted, two that have held, and a small method you can use to audit your own thesis this weekend.

The Reframe

A thesis is not a commitment, it is a working hypothesis. The discipline is not defending it, the discipline is updating it on the right evidence and refusing to update it on the wrong evidence.

Three principles for the rest of this issue.

The thesis you wrote was a hypothesis built on what you knew before searching. Ten months in, you know things you did not.

The right reasons to revise are repeated patterns across multiple data points, real seller behaviour, real financing constraints, real operating realities.

The wrong reasons to revise are one bad deal, one rejection, one bad week, fashion in what other people are buying.

Four dimensions of my own thesis have moved. Here is what moved on each.

1. The Model

In August I was anchored on holdco.

I had spent eighteen months on the topic, including the entire research arc of my MBA thesis on post-acquisition governance in holdco structures. I knew the model. I believed in the model. I still believe holdco is the theoretically best long-term fit for me.

I am not building one.

The reason is capital. A real holdco requires either personal balance sheet I do not yet have, or an investor base I have not yet earned. Without one or the other, “I am building a holdco” is a statement of intent, not a working model. The honest version of where I am is somewhere between two adjacent models: a self-funded search and an independent sponsor structure. I have not yet fully landed between the two. The decision is being shaped in real time by which deals come to me.

Traditional search fund never fitted me. That has not changed.

Holdco is the belief that took me the longest to revise. Eighteen months of academic work makes a model hard to let go of, even when the cap table does not support it. The shift happened gradually, in conversations with European investors who told me directly what a holdco actually requires at this stage in this market, and in my own honest review of what I could fund myself.

The principle for any reader sitting on a similar gap: the model choice should follow the deal access and the capital reality, not the other way round. Picking a model because you wrote a thesis about it is not a thesis decision, it is an identity decision.

2. The Geography

In August I was looking only in the Amsterdam area.

That was the wrong frame.

Today my geography is the Netherlands as a whole, Lower Saxony and North Rhine-Westphalia in Germany, and the Flemish part of Belgium. Three countries, two languages I speak natively, one cultural region I genuinely understand.

The shift came from a sharper question. Not “where can I search” but “where do I match the seller’s culture and the lender’s structure.” The Netherlands works because I live here. The two German states work because I am German, my credit score is German, and the lender ecosystem in those states (Sparkassen, regional banks, KfW-backed financing) is set up for transitions of the size I am targeting. Flemish Belgium works because the language and culture extend the Dutch reach.

What I learned that changed the geography:

European succession deals do not run on the same lender infrastructure across the continent. Each country and sometimes each region has its own credit logic. KfW in Germany, BMKB in the Netherlands, regional development banks in Belgium. If you do not have a credit history in the country, you will struggle to get the financing stack to close, even if the deal is good.

The principle worth keeping: geographic focus narrows as you learn what is actually available. A pan-European thesis sounds impressive on paper and falls apart in the financing call. The honest version is one or two countries deep, not five countries shallow.

3. The Sector

In August I was going to acquire a Dutch accounting firm near Amsterdam, around two million euros in revenue, six to eight hundred thousand EBITDA. The plan was to transform a traditional accounting practice into a modern CFO-services business.

I am no longer pursuing accounting firms.

I want to be honest about how this felt. I spent years in banking and audit. Accounting was the sector I understood best, where my fit was strongest, where my credentials carried weight. Walking away from it felt like sad and disappointing. I would not pretend otherwise.

What moved me was AI exposure. I wrote about this in I Wasted 6 Months in 2025 Part 1. The more I looked at small accounting firms, the more I saw the basic services, bookkeeping, compliance work, standard financial reporting, were already being absorbed by software and AI. The valuation logic of an acquisition is “earnings will hold or grow.” That logic is fragile in a sector where sixty percent of the work can be automated in the next five years.

So I moved. Today my sector focus is blue-collar work, specifically craftsmanship businesses in HVAC, electrical, and fire protection. Three reasons.

They are AI-resistant. You cannot automate a broken pipe in someone’s home, a faulty wiring installation, or a fire-safety inspection.

They are recession-resistant. People still need heat, light, and fire safety even when the economy contracts.

They have a succession wave. In Germany alone, roughly one million businesses need to find a successor by 2030. A meaningful share of them are in exactly these trades.

The principle that travelled across the shift: when you change sector, the credentials you held in the old one mostly do not carry. What carries is the framework you developed for evaluating a sector. AI-resistance and recession-resistance still apply.

4. What you actually want from the business

The least-discussed dimension, and the one that moved most quietly.

In August my picture was a mix of independence, ownership, lifestyle, and financial outcome. I would have said all four mattered, and I would have meant it.

Ten months later the mix is sharper. Independence and ownership and lifestyle have moved up. Lifestyle in the specific sense of being able to work from where I want, spend time with my family, and shape my week. Financial outcome has moved down, not because it does not matter, but because I have learned that if the first three are in place, the financial outcome tends to take care of itself in this asset class, and if they are not in place, no financial outcome justifies the cost.

There is one specific role shift inside that mix worth naming. In August I pictured myself as the operator-CEO inside the business. The buyer, the operator, the leader of the team, all the same person. That picture has moved. I want to own the business, work on it, hire an operator who runs the day-to-day, and shape the strategy rather than execute it. That is a different ambition from the one I started with, and it changes what kind of business I look for. A craftsmanship business with a strong number two already in place is more valuable to me than the same business with the owner doing everything.

The principle for any reader: most searchers run their search against an unexamined mix of motivations. The cleaner the motivations are named, the better the deals you can say no to. A vague “I want freedom” is not a filter. “I want to work from where I live, with people I respect, on something that does not require my hands every day” is a filter.

There is one more thing on this dimension that has shifted recently, and I want to name it briefly.

Ten months ago I was building this alone by default. I no longer think alone is the right model for the next phase. The hybrid model I now think fits me best is one I would build with a partner, someone with operational depth that complements my financial and structural side. If you are thinking similarly, reply and tell me how you see it.

That is the only line of personal news in this issue. I am keeping it short on purpose.

5. Two things that have not changed

Honest balance. Not everything in my thesis has shifted. Two things have held in exactly their original form, and naming them makes the changes credible.

Deal sourcing. My approach has been the same since day one. Personal network, with deliberate relationships into chambers of commerce, local government administrations, and regional development bodies. I do not rely on broker listings as the primary channel. I rely on the people who see succession coming before the listing exists. That has worked, and there is nothing in ten months of searching that has made me want to change it.

Financing method. Bank loan plus investor capital plus skin in the game from me plus available subsidies plus seller financing where the seller is open to it. Five layers, calibrated to each deal. The mix has not changed because the structural reality of European mid-market financing has not changed. KfW in Germany, BMKB in the Netherlands, regional development support across Belgium. These are the rails. If you build a financing stack that uses them well, it holds up.

Those two things have stayed because the evidence has confirmed them, not because I have refused to look. That is the difference.

Recently in Conversation

Two recent conversations have stress-tested some of the thinking in this issue. Different hosts, different audiences, different angles on the same question.

The first was with an American host, framed around how Europe is structurally different from the US. The second was with a German host, framed around how Europe should be organising itself for what is coming. Same person, two different conversations.

Episode 1, Search Funded: The ETA Podcast with Nick Lall

Long-form conversation on how the European ETA reality reshapes the American playbook, recorded for an audience of mostly US searchers and investors.

Three takeaways from the conversation:

Local investors are not optional in Europe. An American investor cannot deploy capital into a European deal without a local lead partner. The local investor base, family offices adapting to ETA, regional firms like Newton Campos, Novastone, Mood Base Capital, and a growing number of smaller European specialists, is now real but still emerging. Cross-border ETA runs on local trust, not on a global playbook.

Regulation is infrastructure, not obstacle. The German Handwerk requires a Meisterbrief, a master certificate, to operate a regulated-trade business. As a non-certified buyer you can hire someone who holds one. If that operator leaves, the local chamber actively helps you find a replacement. This is regulation acting as a support system, not a barrier, and it is one of the structural reasons German craftsmanship is a more interesting acquisition target than most American searchers assume.

The post-acquisition move nobody talks about is hiring the previous owner as a staff member or advisor for three to six months. Conventional wisdom says get the seller out fast. My MBA research interviews with American operators pointed clearly in the other direction. The previous owner knows the suppliers, the clients, the unwritten processes. Three to six months of structured handover is the highest-ROI continuity move available, especially for first-time buyers.

Episode 2, buypreneur Podcast with Timm Wienberg

“Warum Unternehmensnachfolge in Europa vor einem Durchbruch steht” (Why succession in Europe is on the verge of a breakthrough) — a long-form conversation in German on where European ETA stands and how Germany and the Netherlands should be organising for the succession wave.

Three takeaways from the conversation:

The Spanish ETA ecosystem is roughly five years ahead of Germany and the Netherlands, driven by universities running formal ETA tracks and government policy treating succession as economic infrastructure. The lesson is not to copy Spain. The lesson is that institutional attention compounds an ecosystem faster than capital alone.

Investors are quietly shifting their preference from MBA graduates to entrepreneur backgrounds. A Spanish investor at the INSEAD ETA Conference told me directly that he no longer prioritises MBA-only profiles. He wants searchers who have built something, even a small project, even a failed one. Operating experience is becoming the new asymmetry, ahead of pedigree.

The cleanest post-acquisition principle from the American operators I interviewed was “change nothing for the first weeks.” Learn the processes that are already there. Document everything, change nothing. The temptation to act fast in the first ninety days is exactly what breaks acquisitions, because the things you are tempted to change are usually the things you do not yet understand.

This episode is in German. If you do not speak German, the transcript opens directly in YouTube and translates cleanly with Claude or ChatGPT. Or reply to this email and I will share the key parts.

If you have only fifteen minutes, the Newton Campos and previous-owner-as-advisor exchange in the Search Funded episode, and the partner-versus-solo investor preference exchange in the buypreneur episode, are the two moments I am still thinking about.

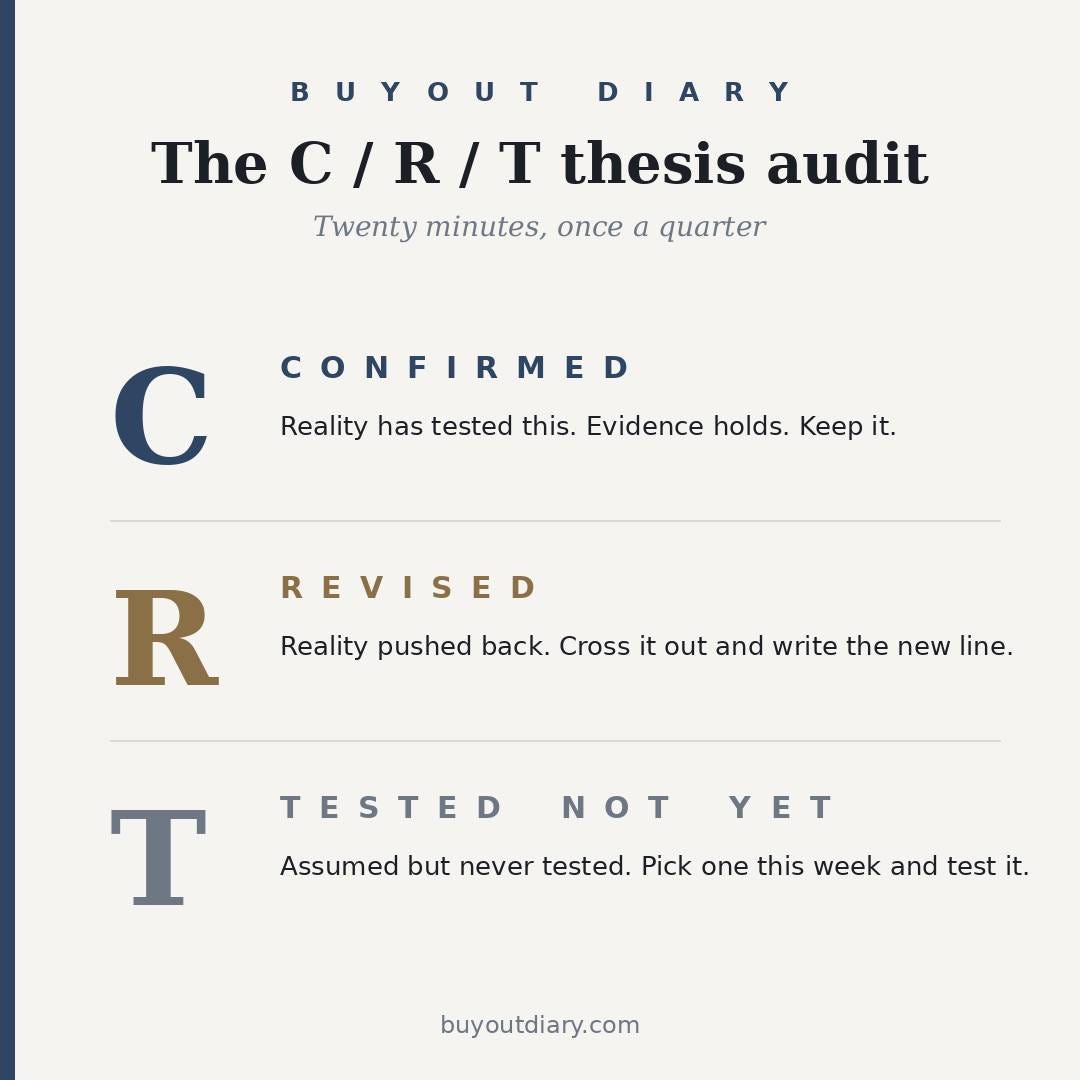

The Audit Method: C, R, T

A practical method you can use on your own thesis this weekend. I call it C / R / T.

Pull out your written thesis from when you started, or write down what you would have said. Read it line by line. Mark every claim with one of three letters.

C, confirmed. Reality has tested this claim and it has held. You have evidence, not just intuition. Keep it.

R, revised. Reality has pushed back on this claim. You believe something different now. Cross it out. Write the new line next to it.

T, tested-not-yet. You have not actually exposed this claim to reality. You assumed it would be true and have not had the chance to test it. Mark it for testing.

The Rs are the work. Every R is a piece of your thesis that has earned its revision. Write the new line out and date it. That is your updated thesis.

The Ts are the warning lights. If too much of your thesis is sitting in T after six months, you are not really searching, you are still writing. Pick one T this week and go test it. A conversation with a real seller, a real lender, a real operator. The thesis is built by the testing, not by the writing.

Twenty minutes, once a quarter. Less than the time you spent writing the original.

What this means for a searcher this week

Three actions scaled by ambition. Pick the one that fits where you are.

Smallest step. Pick one claim in your current thesis and write down the evidence for it. If you cannot, that claim is a belief, not a thesis. Name it as a belief and move on.

Bigger step. Do the full C / R / T audit on your thesis this weekend. One sitting, twenty minutes. Date the new lines so you can audit again in three months.

Boldest step. Share your revised thesis publicly. A LinkedIn post, a note to your investor circle, a paragraph in your next newsletter if you write one. Public revision builds trust faster than initial conviction does, because anyone can have conviction in August. Revision in June is evidence of work.

If you take one thing from this issue, take this.

A thesis that has not moved in ten months is a thesis that has not been tested. Revision is the work. The thesis you started with was built on what you knew before you searched. The thesis you hold now should be built on what you have learned since.

I am self-funded, and the budget is tight. Time is one cost, money is the other, and self-funded means both come from the same person. I am still searching, I have not closed an acquisition, and the willingness to revise has cost me a model I spent eighteen months building. It has given me a sharper sector, a sharper geography, and a clearer picture of what I actually want from the business I eventually own.

Before you go, hit reply and tell me one thing.

What is one belief you used to hold about your search that you have already revised? Tell me in one sentence. The replies become the next issue.

See you next Monday.

Alexander