What a €4.3 billion deal teaches a self-funded buyer

The best acquirers in the world think differently. Here is how.

Hello, and welcome back to Buyout Diary.

On Friday I posted three questions on LinkedIn that apparently hit a nerve. The post generated more saves and replies than anything I have shared in weeks.

The three questions were simple.

Why did the Bulgari family sell a business they had owned for 127 years?

Why did LVMH pay a 61% premium to acquire it?

And what does a €4.3 billion deal teach a self-funded buyer looking at a €2 million business in the Netherlands, Belgium, or northwest Germany?

This issue answers all three in considerably more depth than a LinkedIn post allows.

The last issue of Buyout Diary was the structural argument, why US frameworks fail in Europe and what a genuinely European acquisition playbook looks like.

This issue shifts register. It is not about my search, and it is not about the European market in aggregate. It is about how the greatest acquirer in the world actually thinks about buying a business, and what happens when you study that thinking carefully enough to extract something useful for the deals the rest of us are doing at a fraction of the scale.

Bernard Arnault has completed more than 75 acquisitions across six decades. He has built the world’s most valuable luxury conglomerate not by being the most aggressive buyer in the room, but by being the most patient, the most deliberate, and the most consistent in his understanding of what a business is actually worth and who it deserves to become. If you want to understand how the best acquisitions are made; the philosophy, the mechanics, the patience, studying him is the most efficient path I have found.

This is Part 1 of a series I am running called Luxury Lessons in Acquisition Entrepreneurship. It will appear across several issues of this newsletter over the coming weeks, interspersed with other content. There are four parts in total: two on BVLGARI, two on Tiffany & Co. Each covers a different phase of what Arnault does — the search, the courtship, the deal structure, the integration.

We start with BVLGARI. The search. The courtship. The deal.

1. The Art of the Patient Buyer

There is a distinction that separates most buyers from the best ones, and it rarely appears in any acquisition primer. Most buyers treat a deal as a transaction to be executed. They define their criteria, identify a target, run their financial analysis, make an offer, negotiate the terms, and close. The process is logical, sequential, and efficient. It is also the reason most buyers end up competing on price with everyone else who is running the same process.

Bernard Arnault treats a deal as a relationship that has not yet found its moment. That is not a rhetorical flourish. It is a description of how he actually operates. He identifies businesses he considers exceptional years before he approaches them. He builds relationships with the families and founders who own them. He waits until the conditions are right, until the seller is ready for a conversation that is genuinely about what comes next, not about price. And then he moves with precision.

The BVLGARI acquisition, announced on 7 March 2011 and valued at €4.3 billion, was not the result of a formal sale process. It was the result of years of attention and relationship-building that made Arnault the obvious and trusted counterpart when the Bulgari family was finally ready to think about what came after family ownership. By the time the deal was announced, most of the difficult work had already been done outside the negotiating room.

Underneath that observation sits a second one, which I think is more important for the kind of buyer most readers of this newsletter are becoming. Arnault did not buy BVLGARI to sell it. He bought it to own it permanently — the way the Bulgari family had owned it for the 127 years before him. That commitment to permanence, to building something that compounds over decades rather than optimising for a multiple at exit, shapes every decision he makes downstream. How he searches, how he approaches sellers, how he structures deals, and how he thinks about the price he is willing to pay.

When I think about my own search, the buyer I am trying to become is this one. Not the buyer who screens for the fastest path to a return. The buyer who asks whether this is a business worth being responsible for in thirty years.

Arnault is the proof that this approach works at scale. BVLGARI is the case study that shows exactly how it works in practice.

What if small business buyers approached deals the way Arnault approached brands — not as assets, but as legacies to steward?

That is the question this issue is built around.

2. The Search: Buy Excellence, Not Distress

BVLGARI was founded in 1884 by Sotirios Voulgaris, an Ottoman-born Greek silversmith who moved to Rome and opened a small shop selling silver goods and antiques. By 1905, the family had established themselves at Via Condotti, the most prestigious shopping street in Rome, and the brand had begun its slow transformation from artisan shop to luxury house.

Over the next century, the Bulgari family built something extraordinary. Not through marketing or financial engineering. Through craft, consistency, and an obsessive focus on design. Paolo Bulgari, the Chairman who would eventually negotiate the sale to LVMH, spent decades personally supervising the design team from an office with a glass door directly into the studio. He was still doing it into his seventies.

Francesco Trapani, Paolo’s nephew and CEO since 1984, had taken the business from a €25 million jewellery company with five stores and 80 employees to a genuine global luxury brand. By 2011, BVLGARI was generating approximately €1.5 billion in annual revenue across jewellery, watches, fragrances, leather goods, and hotels. It had 300 stores and 4,000 employees. Trapani had listed the company on the Milan Stock Exchange in 1995, expanded into Bulgari Hotels and Resorts through a joint venture with Marriott in 2001, and built a fragrance business from scratch that by the mid-nineties was generating over $40 million annually.

The business was genuinely exceptional. But it was not without pressure.

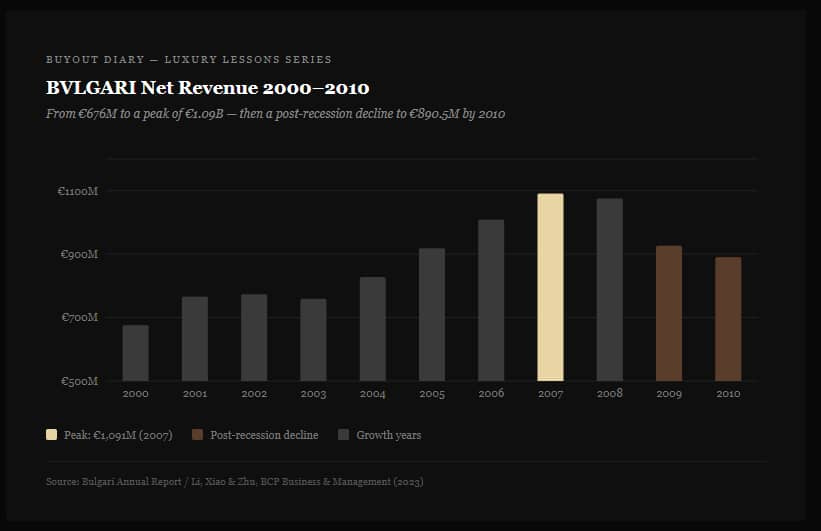

The 2008 recession had hit BVLGARI hard. Net revenue had declined steadily from €1.091 billion in 2007 to €890.5 million in 2010. The brand had made significant store investments during that same period of falling sales — expanding the retail footprint while cash flow was shrinking. The financial muscle needed to grow at the pace the brand deserved was simply not there.

This is the nuance most buyers miss when they study Arnault’s acquisitions. They assume he was buying either distressed assets he could fix cheaply, or perfect businesses he overpaid for. The reality is more interesting. He consistently finds the business that is structurally exceptional but operationally constrained by factors the right owner can remove. BVLGARI was not failing. It was limited. And the thing limiting it — scale, capital, and global distribution — was exactly what LVMH had in abundance.

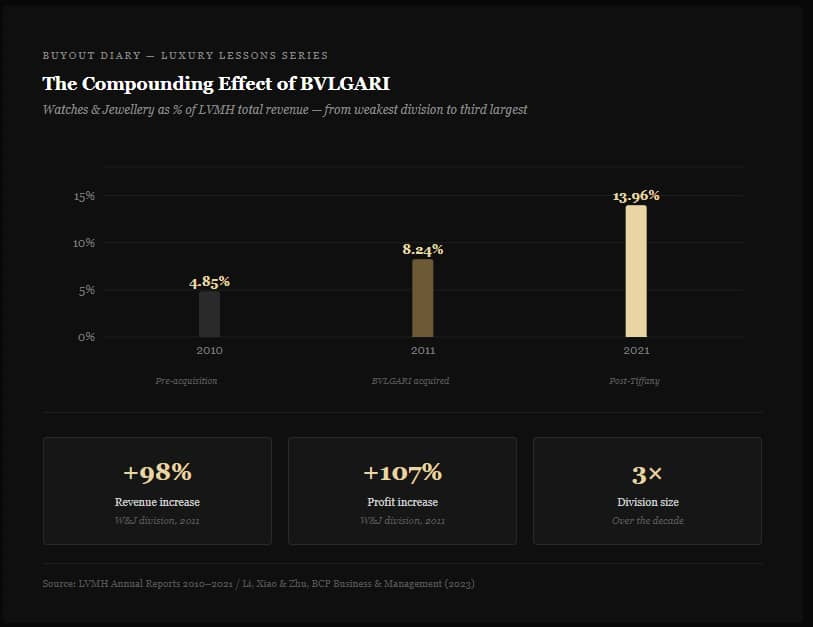

LVMH by 2011 was dominant in fashion, leather goods, wines and spirits, and perfumes. Its watches and jewellery division, established only in 1999 through the acquisitions of Chaumet, Zenith, and Tag Heuer, was the weakest part of the portfolio by a considerable margin. In 2010, only 4.85% of LVMH’s total gross revenue came from Watches and Jewellery — the smallest share of any business group. The division lacked a jewellery maison with genuine heritage and global brand recognition. That was the gap. And Arnault had identified BVLGARI as the business that could close it.

The gap analysis he was running was precise. LVMH strong in fashion and leather. LVMH weak in jewellery. BVLGARI strong in jewellery heritage and brand. BVLGARI constrained by the capital, retail infrastructure, and global distribution network it needed to grow. One side of the table had the brand. The other side had the platform. Together they were worth considerably more than either was separately.

The ETA parallel: Strategic search beats opportunistic search. The buyer who spends six months understanding a single sector deeply — who the best operators are, what the structural growth drivers are, where the succession gaps sit — will consistently find better businesses than the buyer screening 200 opportunities for the most obvious metrics. Criteria matter. But understanding what makes a business genuinely excellent, and finding the rare ones that qualify, is the real search.

3. The Courtship and Trust-Building

Francesco Trapani said something after the deal closed that reveals everything about how Arnault operates. Speaking to WWD, he said:

“We were not ready to sell. We wanted to remain entrepreneurs. We were not looking to retire and cash out. We were not ready to sell, but to change the profile of our entrepreneurial activity.”

The Bulgari family had been approached over the years by the majority of major luxury companies about a possible combination. They turned them all down. Not because the prices were wrong. Because the buyers were wrong.

Other buyers wanted full control. They were, in Trapani’s words, afraid of losing control, especially Italians who are jealous of their companies. They approached the Bulgari family as sellers of an asset. They got negotiations that went nowhere.

Arnault approached them as partners in a next chapter.

The difference was not the price. It was the framing entirely. LVMH was not buying BVLGARI. LVMH and BVLGARI were joining forces to do together what neither could do as well alone. The Bulgari family would become the second largest family shareholders in LVMH, behind only the Arnaults themselves. Paolo and Nicola Bulgari would remain Chairman and Vice Chairman of the BVLGARI board. Trapani would lead the enlarged watches and jewellery division across the whole LVMH group. The family’s entrepreneurial identity would be preserved rather than absorbed.

That framing only works if you have spent years building the relationship that makes it credible. You cannot walk into a first meeting and tell a 127-year-old family that you respect their legacy and expect them to believe you. The relationship has to precede the claim.

Arnault does not negotiate trust. He builds it steadily over time before he ever needs it. By the time a deal conversation begins, the seller already knows who he is, how he operates, and what his businesses look like after five years inside LVMH. The negotiation is almost a formality at that point.

This is cultural diplomacy as much as it is business strategy. No hostile takeover. No auction. No process that forces the family into a position where they are choosing between competing bids and optimising for the highest number. Instead, a quiet relationship built over years that eventually finds its natural moment.

Arnault’s empathy in founder transitions is one of his most underappreciated skills. He understands that a founder selling a business they have spent decades building is not primarily thinking about the price. They are thinking about their employees, their customers, the community around their business, and whether the buyer will honour what they spent their life creating. The buyer who addresses those concerns directly, before the price conversation begins, consistently wins deals that the buyer focused only on valuation cannot reach.

The ETA parallel: In European ETA, the seller who is three years from retirement is worth knowing now. The business owner in Europe who has spent forty years building something will not respond to a cold approach with a criteria document and an acquisition process. He will respond to someone he has seen consistently, who has shown genuine interest in what he built, who has demonstrated over time that they think about ownership the way he does. The courtship is not a step in the process. It is the process.

4. The Deal Structure: Alignment Over Control

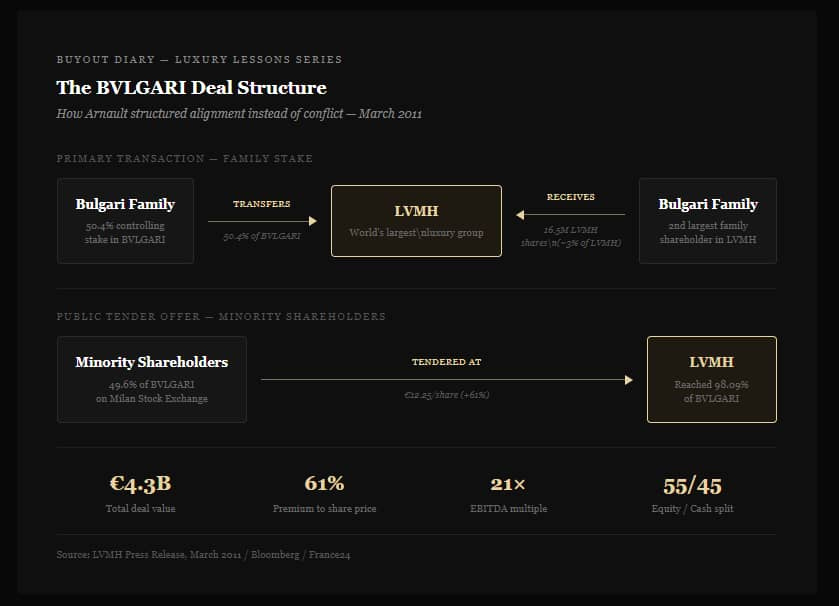

On 7 March 2011, LVMH announced the acquisition of BVLGARI in a deal valued at approximately €4.3 billion. The mechanics of how that deal was structured are worth examining in detail, because they reveal something important about how Arnault thinks.

LVMH acquired the Bulgari family’s 50.4% controlling stake through a share exchange. In return for the family’s entire stake in BVLGARI, they received 16.5 million LVMH shares, giving them approximately 3% of the world’s largest luxury group. This was not a cash buyout. The Bulgari family did not take their chips off the table and retire. They exchanged their ownership of one exceptional business for a meaningful stake in the broader empire it was joining.

The deal was financed approximately 55% with LVMH equity and 45% with cash. For the remaining minority shareholders who were not part of the family’s share swap, LVMH made a public tender offer at €12.25 per share. By October 2011, BVLGARI was delisted from the Milan Stock Exchange and LVMH owned 98% of the company.

The implications of that structure are significant on three levels.

First, it created genuine alignment. The Bulgari family were now LVMH shareholders. Their personal wealth was directly tied to the performance of the broader group, which depended partly on what BVLGARI became under LVMH management. They had every reason to make the integration work because they were not exiting. They were continuing in a different form, with far greater resources behind them.

Second, it solved the seller’s real problem rather than the buyer’s assumed one. The family had said explicitly they did not want to retire or cash out. A standard cash buyout would have handed them liquidity they did not need and removed them from the entrepreneurial world they had spent their lives in. The share swap gave them capital appreciation as LVMH grew, continued relevance inside one of the world’s most prestigious businesses, and seats on the LVMH board. It addressed what they actually needed.

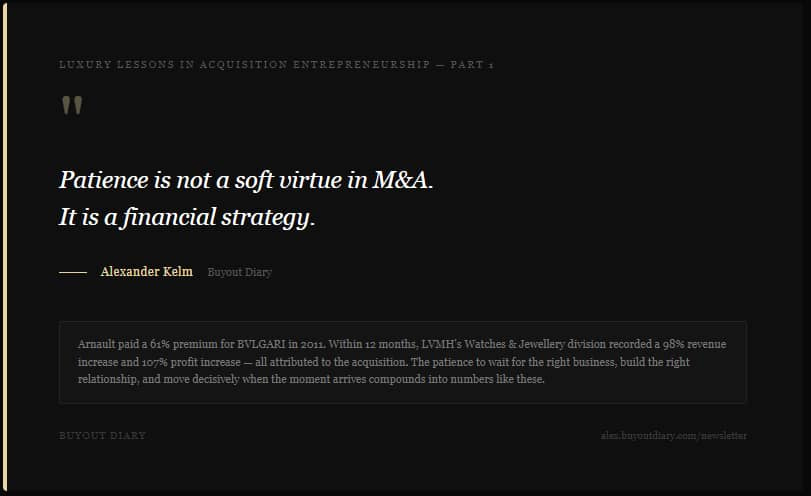

Third, the price itself was significant. The offer of €12.25 per share represented a 61% premium over BVLGARI’s closing price the Friday before the announcement. Analysts at the time valued the deal at approximately 21 times EBITDA, well above typical M&A benchmarks. One analyst noted the price seemed hefty by general M&A guidelines. Arnault paid it anyway.

He paid it because he was not buying the trailing EBITDA. He was buying what BVLGARI could become with LVMH’s capital, retail network, and global distribution infrastructure behind it. The premium reflected the gap between what the business was worth in the hands of a family constrained by post-recession cash flow and what it was worth inside the world’s largest luxury group. That gap was real. The numbers proved it immediately.

In the year of acquisition alone, LVMH’s Watches and Jewellery division recorded a 98% increase in revenue and a 107% increase in profit. The division’s share of LVMH’s total gross revenue jumped from 4.85% in 2010 to 8.24% in 2011. Every euro of that growth was attributed to the consolidation of BVLGARI. The year after, the division continued to record a 46% revenue increase and a 26% profit increase, exceeding every other LVMH business group in growth rate. The 61% premium Arnault paid looked expensive on the day of the announcement. It looked rational within twelve months.

The Bulgari family subsequently became the second largest family shareholder in LVMH behind the Arnaults. The relationship that had begun as a negotiation became a genuine long-term alignment of interests.

The ETA parallel: Creative deal structures create alignment. A seller note is not a weakness in a deal. It is a way of keeping the seller financially invested in a successful transition. An earn-out bridges a valuation gap while giving the seller continued upside tied to performance. A rollover equity arrangement gives the former owner a reason to support the new buyer’s success rather than simply counting their cash and moving on. The best European deals are rarely clean cash transactions at full price. They are structures that answer the seller’s real question honestly: will I be better off after this than before?

5. Negotiation Dynamics: Calm Leverage Wins

One of the most remarkable facts about the BVLGARI deal is how quietly it was assembled.

There was no formal auction. No investment bank running a competitive sale process. No multiple rounds of bidding. The deal was concluded over a single weekend. The LVMH board approved it Sunday evening. The Bulgari board approved it simultaneously. The announcement came Monday morning. Years of relationship-building compressed into 48 hours of execution.

How does that happen?

Arnault’s leverage in every major negotiation comes from the same source. He is not the most aggressive buyer. He is the most patient one. He does not need any single deal. He has built a portfolio so strong and a reputation so consistent that sellers come to him — or when they are reluctant, they find him easier to say yes to than any alternative.

Trapani described the dynamic clearly. He had spoken with the majority of major luxury companies over the years about a possible combination. Most wanted full control. Most were unwilling to structure a deal that preserved the family’s entrepreneurial identity. LVMH was willing. That willingness, demonstrated through years of consistent behaviour rather than promised in a negotiation, is what made Arnault the obvious counterpart when the Bulgari family was finally ready to move.

This is soft power in M&A. Trust built over time rather than tactics deployed in the room. Reputation accumulated through how previous acquisitions were handled rather than promises made in this one. The families behind Dior, Givenchy, Céline, and Louis Vuitton had all experienced LVMH integration from the inside. Their experience was the most persuasive testimony Arnault could offer to any new seller.

Emotional discipline in a negotiation is the practical expression of this philosophy. The buyer who needs to close a specific deal will always pay more than the buyer who is genuinely willing to walk away. Arnault knew his financial position well enough to act with confidence when the moment arrived. LVMH’s debt-to-equity ratio at the time was just 16% and free cash flow exceeded €4 billion annually. He could move decisively because he had prepared deliberately.

He also moved at the right moment in BVLGARI’s history. The business was growing strongly but the family was at a natural inflection point in its generational transition. The succession question that faces every family business eventually was beginning to make itself felt. Arnault understood the timing. He was ready before the window opened.

The ETA parallel: Build a pipeline of relationships before you need them, not deals. A searcher who has been having genuine conversations with owners, advisors, and accountants for eighteen months will close deals that the searcher who starts outreach the day they are ready to buy will not reach. You cannot manufacture calm leverage in a negotiation. You can only build it in advance.

6. Five Lessons for Every Acquisition Entrepreneur

The BVLGARI acquisition is not just a good story about a famous deal. It is a manual for how to think about buying a business when you are playing a long game. The lessons apply at every deal size.

Build relationships before deals. Arnault did not approach the Bulgari family when he was ready to buy. He built a relationship with people he respected over years. When the moment came, the trust was already there. In European ETA, the seller who is three years from retirement is worth knowing today.

Buy excellence, not distress. The conventional search for underperforming assets with obvious operational fixes is one approach. The more durable approach is finding businesses that are genuinely excellent and asking what they could become with the right owner and the right resources behind them. Excellence is rarer and more defensible than operational improvement. It is also harder to find, which is why most buyers never look for it properly.

Structure alignment, not control. The equity swap that made the Bulgari family LVMH shareholders was not accidental. It was the structure that answered what they actually needed. Every deal has a structure that serves both parties better than the default cash transaction. Finding it requires understanding what the seller is actually afraid of losing, not just what the buyer wants to acquire.

Respect the legacy when buying founder-led firms. The businesses that come with the deepest succession opportunities in European ETA are founder-led. They carry the values, relationships, and culture of the person who built them. The buyer who treats that as an obstacle to be managed will destroy value the moment the founder leaves. The buyer who treats it as the core of what they are acquiring will compound it.

Think in decades, not exits. Arnault did not buy BVLGARI to sell it in five years. He bought it to build it into the global jewellery leader it has since become. Over the decade following the acquisition, LVMH’s Watches and Jewellery division tripled in size. By 2021 it accounted for 13.96% of LVMH’s €64 billion in total revenue, exceeding Wines and Spirits and Perfumes and Cosmetics, and sitting as the third largest business group in the empire. That long-term orientation shapes how Arnault approaches every part of a deal. For self-funded buyers in Europe, the same logic applies. The best SME acquisitions are not exit plays. They are compounding machines. The patience to wait for the right business, build the right relationship, and move decisively when the moment arrives is not a soft virtue. It is a financial strategy.

Coming Up in the Series

The deal is closed. The Bulgari family are still in the building. Paolo and Nicola remain Chairman and Vice Chairman. Trapani is now running LVMH’s entire watches and jewellery division.

Now comes the part most acquirers get wrong.

How do you integrate a 127-year-old Italian family business into the world’s largest luxury group without destroying what made it worth acquiring in the first place?

How do you give a newly acquired business enough autonomy to preserve its identity while ensuring it performs against the expectations that justified the premium?

And what does Arnault’s answer to those questions teach a self-funded buyer handing over the keys to a 15-person business in the Netherlands or Belgium?

Part 2 of this series — BVLGARI: The Integration Playbook will appear in a coming issue of Buyout Diary. There will be other content in between, as always. But this thread will continue.

See you next Monday.

Alexander