Why LOIs break even when diligence is clean

Most LOIs do not break on a single number. They break on confidence eroding across four dimensions at once.

Hello, and welcome back to Buyout Diary.

This issue starts with a question from a reader.

In a recent newsletter issue I wrote openly about being nine months into the search, two LOIs signed, two LOIs broken, no deal closed. A reader replied with one of the sharpest questions I have received since the newsletter began.

“Why do LOIs break when due diligence is clean?”

The reader is Veena Giridhar Gopal, Managing Director of New Chapter Capital and a Novastone-backed searcher. Her LinkedIn and Novastone profile are public. She is not a hypothetical reader, she is in the deal flow, working through the same questions every active searcher works through.

Her question named the situation almost every serious searcher will face at least once. The legal review is clean. The numbers check out. The Quality of Earnings is reasonable. And the deal still does not close.

The instinct is to find one reason. The seller got cold feet. The bank pulled back. The lawyer found a clause. But that is rarely what actually happened.

The honest answer is that LOIs almost never break on a single number. They break on confidence eroding across multiple dimensions at the same time. The diligence is one of those dimensions. There are three others, and they are usually the ones that move first.

The Reframe

A clean LOI does not mean a clean path to close. An LOI is a snapshot of mutual confidence at one moment. Closing requires that confidence to hold across roughly six to twelve weeks of diligence, financing, and re-negotiation. That is a long time for confidence to hold.

This is not a niche phenomenon. The Stanford Graduate School of Business 2024 Search Fund Study found that of search funds that concluded their search, only 63 percent made an acquisition, down from 66 percent in 2022. Roughly four in ten searchers who run their search to its end do not acquire. Veena’s question sits in the middle of that gap.

The pattern is studied, not random. S&P Global Quantamental Research built a predictive model of deal cancellation from four identifiable drivers, forecasting cancellation rates at roughly twice the base rate. Broken deals have signal, not just noise. The question is which signals to watch.

Four dimensions of confidence have to stay roughly stable for the deal to close. When two or more start to drift, the deal usually breaks, even if the technical work all checks out.

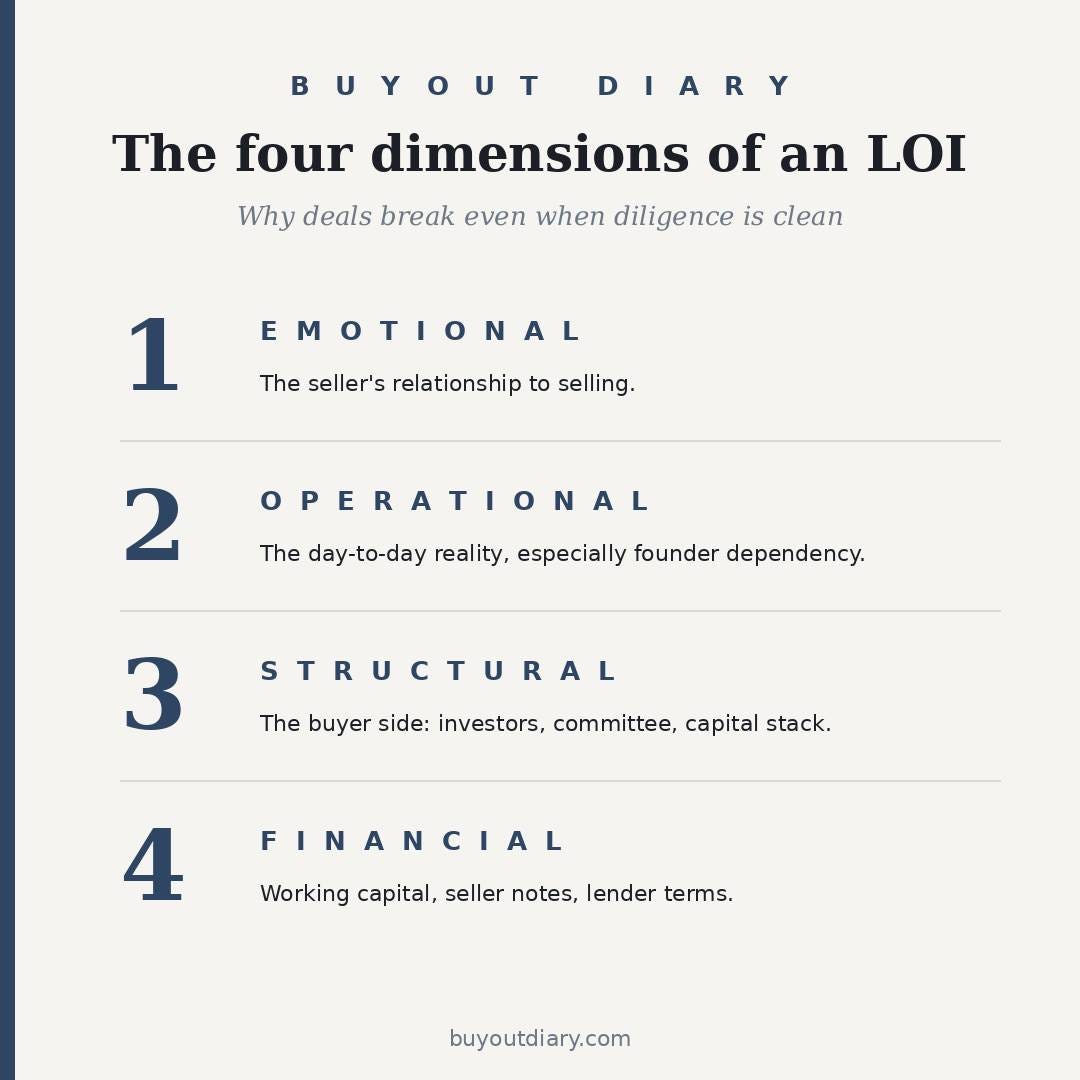

The four dimensions:

1. Emotional. The seller’s relationship to selling.

2. Operational. The day-to-day reality of the business, especially founder dependency.

3. Structural. The buyer side: investors, committee, capital stack.

4. Financial. The financing layer: working capital, seller notes, lender terms.

Each one walked through in the next four sections.

What the Research shows

63 percent. Acquisition rate among Stanford-tracked search funds that concluded their search, down from 66 percent in 2022. Source: Stanford GSB 2024 Search Fund Study.

3.6 LOIs to close. Average number of letters of intent signed per closing searcher, with the first signed 7.8 months into the search. The IESE 2024 International Search Funds Study, tracking 320 international funds, reported a comparable average of approximately four LOIs to close. Self-funded searchers specifically averaged 2.4 LOIs, per the SIG Self-Funded Search Study. Sources: Stanford GSB 2024; IESE 2024; SIG Self-Funded Study.

Four identifiable drivers. S&P Global Quantamental Research found that deal cancellation is predictable from a small set of factors, forecasting cancellation rates at roughly twice the base rate. Source: Oyeniyi and Tortoriello, S&P Global, February 2018.

1. Seller emotional drift

The seller signed the LOI for one set of reasons. Six weeks into diligence, those reasons may not look the same.

I have not lived this pattern myself. My own two broken LOIs were not driven by seller emotional drift. But I have seen it in other searchers’ deals, and it shows up in almost every conversation I have had with experienced operators about why their first acquisition took longer than they thought.

What changes for the seller emotionally during diligence:

The price stops feeling abstract and starts feeling concrete (often smaller than imagined)

Long-term relationships (employees, suppliers, customers) start to feel like things being handed over rather than things being kept

The post-sale identity question lands: who am I when I am not running this business?

A spouse, partner, or trusted advisor weighs in

A competitor or a different buyer makes a parallel approach

What the buyer can see (and often misses):

Slower response times to emails

Reduced eagerness to provide documents

New “small” objections that were not raised at LOI

A return to the “but I might want to stay involved” conversation

The seller starting to talk about the business as if they are not selling it

One adjacent pattern I have seen: the seller who quietly raises their price during diligence, sometimes by ten or fifteen percent. Diligence has not found anything wrong with the business. The seller has just decided their business is worth more than they thought when they signed the LOI. That is emotional drift disguised as price negotiation.

The principle: emotional drift is detectable two to four weeks before it becomes a break. The buyer who notices early can either save the deal by re-engaging the relationship directly, or walk away cleanly before more diligence cost is spent. The buyer who is not paying attention finds out at the worst moment.

2. Operational reality, especially founder dependency

This is the pattern that broke both of my LOIs.

Diligence finds what diligence is designed to find. It finds the numbers, the contracts, the legal structure, the financial reporting. What it often misses is the unwritten operational reality: how much of the business actually lives in the founder’s head, their relationships, and their daily decisions.

On both of my broken deals, the issue was founder dependency. The first was deeper than the second. In one of them, the business was so dependent on the founder that the moment you tried to model the business without the founder, the revenue curve started to bend. Not because the business was failing. Because the business was effectively the founder, with a small team supporting them.

This is not unusual. In small and mid-market acquisitions, founder dependency is the rule, not the exception. The work is not to find a business without founder dependency. The work is to understand whether the dependency is repairable in the first ninety days, the first year, or never.

What surfaces during operational diligence that breaks deals:

Founder dependency the numbers did not show (one or two customers who buy because they trust the owner, not the business)

Team intentions that emerge in side conversations (the COO who plans to leave once the founder leaves)

Customer concentration risks the metrics did not capture (one customer who is twelve percent of revenue but sixty percent of relationships)

Processes that look small in isolation but multiply across the first hundred days of ownership

Customer concentration is its own version of founder dependency. If thirty-five percent of revenue comes from one customer, the business has the same fragility as a founder-dependent business, just with the dependency transferred to a third party. Diligence can flag the percentage. Whether the relationship survives the handover is a separate question that requires real conversation with that customer, ideally before signing the LOI.

The principle: diligence is necessary but not sufficient. The buyer who treats diligence as the test of the business will be surprised. The buyer who treats diligence as a starting point for understanding the business will see what diligence missed.

3. Structural pressure on the buyer side

For a self-funded searcher this dimension may sound small. It is not.

The cleanest illustration I have seen of this pattern came from a searcher I know. The deal broke not because of the seller and not because of diligence. It broke because an investor on the equity side dropped out late, and the equity gap that opened could not be closed quickly enough to hold the deal together. The seller did not want to wait. The other investors could not increase their commitment fast enough. The deal closed cleanly on paper but the financing structure unravelled in the last two weeks.

For an institutional searcher, a search fund with a committee, or an independent sponsor with multiple capital partners, this dimension is often the largest hidden risk. The conversations a searcher has informally with a potential investor look reasonable in February. The conversations that same investor has with their own investment committee in April look different.

What changes in the structural conversation:

Committee members ask questions the original sponsor did not anticipate

Co-investors push for terms that the lead investor had soft-committed against

Risk-weighting shifts as the macro environment moves between LOI and close

A lead investor’s portfolio rebalancing forces a smaller cheque

Reputational considerations surface that did not appear in earlier conversations

The principle: the buyer side of the deal is not one person, it is a system. The system has its own confidence dynamics, and they often run slower than the seller side. By the time the system has decided, the seller has moved on.

4. The financing layer

I want to be honest about this dimension. When I first thought about why LOIs break in Europe, I assumed the financing layer would be a specifically European story: working capital adjustments, seller notes, bank loans, lender requirements. Looking at my own deals, that framing was too narrow. Working capital is calculated everywhere. Seller notes are a feature of small-business deals globally, not a European specialism.

What is true across geographies is that the financing layer is the dimension where small surprises compound. Each adjustment chips away at the seller’s confidence in the deal.

What surfaces in the financing conversation:

A seller who expected most or all cash at close, who now sees the seller note in writing

A working capital adjustment the seller did not realise would reduce their proceeds

Tax treatment that turns out worse than the seller’s accountant had hoped

Lender requirements (personal guarantees, covenants, security) that change the seller’s view of the buyer’s commitment

A guarantee or subsidy programme that adds time and paperwork the seller did not expect

In Europe specifically, bank loans and lender-led financing often add weeks the seller had not budgeted for. That is not a structural barrier, it is a timing issue, but a deal under emotional strain on the seller side does not tolerate added weeks.

The principle: the financial structure of a deal is not negotiated once and signed at close. It is negotiated continuously, and each adjustment is a small confidence cost. The buyer who frontloads the harder financing conversations loses fewer deals at the back end.

The pattern across all four

LOIs almost never break on one dimension. They break when two or three drift at the same time.

Both of my broken LOIs had founder dependency as the root issue, which sits in Pattern 2 (operational reality). The operational reality became visible during diligence, and on both deals it was significant enough that the deal could not survive it. Pattern 3 (structural pressure) was not my own story, but I have watched it close deals for other searchers, and the speed at which it can unravel a deal is sobering.

The patterns interact. The buyer’s job during the six to twelve weeks between LOI and close is not just to complete diligence. It is to monitor confidence on all four dimensions and act when one starts to slip.

Any single dimension drifting is recoverable. Two drifting at once usually is not.

A method: score your deals 1 to 5

A practical exercise the reader can do on a current deal or on a deal that has already broken.

Take the deal. For each of the four dimensions (emotional, operational, structural, financial), score on a scale of one to five how stable the confidence currently is, with honest evidence next to each score.

5: rock solid, no slippage detectable

4: confident with one minor flag

3: noticeable drift, action needed this week

2: serious drift, deal is in real risk

1: this dimension has effectively broken

Any dimension at 3 or below is a flag. Two dimensions at 3 or below is a warning. Three or four at 3 or below means the deal is already broken and the buyer has not yet accepted it.

For a deal that has already broken: do the same exercise retrospectively. Where did each dimension actually sit at the moment things changed? The post-mortem is where the next deal gets saved.

Talk to the people around the business

This is the single most important practical thing I would tell a searcher in current diligence on a deal.

Do not just talk to the seller. Talk to the people around the business.

The suppliers. The customers. The local chamber of commerce. The local administration. The competitors if you can. The local industry network. Other business owners in the same town who may have shared a supplier, a customer, a banker.

Why this matters: diligence asks the seller and the seller’s advisors about the business. The seller, by definition, knows the version of the business they have decided to present. The people around the business know a different version. They see the late payments to suppliers that did not make it into the management accounts. They see the customer complaint patterns the team has not surfaced. They see the founder’s reputation in the local market, which is the asset you are about to buy.

A specific version of this advice: ask three suppliers and three customers, separately, one open question. “What has it been like working with this business?” Then say nothing. Listen for at least sixty seconds. The texture of the answer tells you more about the business than the financial statements do.

You also need to check the person, not just the business. Background checks on the seller, on the management team if there is one, on any operator who would stay post-acquisition. Reputation in the city, image in the industry. These are not nice-to-haves. They are part of what you are buying.

This is the work most searchers do not do because it is unglamorous, it takes time, and the answers are unstructured. The searchers who do it find out things that diligence will never find, and they walk away from deals that look clean on paper but smell wrong in the local market.

What you can do this week

Three actions scaled by ambition. Pick the one that fits where you are.

Smallest step. Take one current or recent deal and write down where each of the four dimensions was at LOI versus at break (or now, if it is still live). Just the diagnosis. No action yet.

Bigger step. If a deal is currently live, schedule a fifteen-minute call with the seller this week with no diligence agenda. Just to listen. Ask one question: “How are you feeling about the process so far?” Then say nothing for sixty seconds.

Boldest step. Talk to three suppliers and three customers of the business you are about to acquire, before signing the next LOI. Separately. Same open question. The conversations will change what you sign.

What I have learned, and the close

Veena’s question reframed: a clean diligence is necessary but not sufficient. The clean LOI promises something the closing process has to keep delivering across four dimensions and several weeks.

My own two broken LOIs were not failures of diligence. They were failures to investigate the founder dependency deeply enough before signing the LOI. The other dimensions still mattered, just not as the primary breaking point on my own deals. Naming that is the only way to do better next time.

One last data point worth carrying out of this issue. The Stanford 2024 Search Fund Study found that searchers who close acquire on average their 3.6th signed LOI, with the first LOI signed 7.8 months into the search. The IESE 2024 International Search Funds Study, the European reference covering 320 international funds, found a comparable average of approximately four LOIs to close. Self-funded searchers specifically close on roughly the 2.4th, per the SIG study. So if you have broken one or two LOIs, you are at the median, not behind it. The work is not to break fewer. The work is to read the signals earlier on each one, so the ones that should break, break cheaper, and the ones that should close, close.

What I would do differently on the next LOI: never give up, write down why every LOI broke before signing the next one, and treat the surroundings check as part of the diligence, not an add-on.

Before you go, hit reply and tell me one thing.

If you have had an LOI break or wobble, which of the four dimensions was the first to drift?

I read every reply, and the patterns become the next issue.

See you next Monday.

Alexander