How Arnault integrated BVLGARI without destroying what made it valuable

The post-acquisition playbook most buyers never build

Hello, and welcome back to Buyout Diary.

If you missed Part 1 of this series, the short version is this. In March 2011, Bernard Arnault acquired BVLGARI for €4.3 billion in an all-stock deal that gave the Bulgari family 3% of LVMH in exchange for their controlling stake. He paid a 61% premium. He did it without a formal auction process. And within twelve months, LVMH’s Watches and Jewellery division had recorded a 98% revenue increase and a 107% profit increase, all attributed to that single acquisition.

Part 1 was about how Arnault found, courted, and structured the deal. This issue is about what he did next.

Because the deal is the easy part. The integration is where most acquisitions fail, or where they quietly become something far better than anyone expected.

1. What Happens After You Buy

Most buyers spend months preparing for the close. The due diligence, the financing, the negotiation, the legal process, the announcement. And then the deal closes, the lawyers leave the room, and the real work begins. This is the moment most buyers are least prepared for.

Bernard Arnault does not obsess over the close. He obsesses over what comes after it.

This is not a philosophical distinction. It is a structural one. LVMH’s entire acquisition model is built around the assumption that buying a business is the beginning of a decades-long relationship, not the conclusion of a transaction. Every decision Arnault makes in a negotiation, including the structure, the price, the leadership arrangements, and the governance commitments, is made in service of what happens in the years that follow. He is not optimising for the best deal terms. He is optimising for the best integration conditions.

The BVLGARI integration between 2011 and 2014 is one of the clearest examples of this philosophy in action. A 127-year-old Italian family business, with a deeply ingrained culture, a founding family that had not relinquished operational involvement, a global retail footprint that needed urgent investment, and a brand identity that was both its greatest asset and its most fragile one, all absorbed into the world’s largest luxury conglomerate without a single public stumble.

How Arnault managed that tells you more about his model than the deal itself.

2. The Governance Model: Autonomy With Accountability

To understand how LVMH integrates businesses without destroying them, you have to understand the structure Arnault has built at the holding company level.

LVMH operates what it describes as a decentralised, federated model. Across more than 75 maisons spanning fashion, spirits, cosmetics, watches, jewellery, and selective retailing, each brand operates with significant autonomy. It has its own management team, its own creative direction, its own product strategy, and its own profit and loss account. The holding company does not impose a unified aesthetic, a shared product roadmap, or a centralised creative process. What it does provide is capital, distribution infrastructure, global purchasing power, and operational expertise that no individual brand could replicate on its own.

The governing principle is straightforward: autonomy with accountability. Each maison is trusted to run its own business. Each is held accountable for its financial performance. LVMH neither micromanages the creative process nor ignores the commercial results.

When the BVLGARI combination was announced, LVMH was explicit about its intentions. The formal technical documentation stated that LVMH intended to preserve the identity and autonomy of the Bulgari group and the values which had contributed to the great success of the Bulgari name. This was not marketing language. It was a governance commitment embedded in the combination agreement itself.

For Arnault, this commitment is both ethical and commercial. Ethical because he understands that what makes a luxury brand valuable, its history, its craft, its cultural identity, cannot be manufactured or replaced once destroyed. Commercial because the premium LVMH paid for BVLGARI was precisely a premium for those qualities. Destroying them post-acquisition would be destroying the thing he paid for.

This is the insight that most acquisition buyers eventually learn the hard way. The business you acquire has value because of how it operates. Change how it operates too quickly and you may be left with the shell of what you paid for.

The ETA parallel: In my MBA research on post-acquisition governance in HoldCo-style acquisitions, one of the clearest findings was that most successful acquirers adopt a hybrid approach: combining informal trust with lightweight formal mechanisms, and adapting governance to the maturity of the business and the operator rather than imposing a fixed template from the outside. That is precisely what LVMH does at scale. The federated model is not a rigid system. It is a framework that flexes around each maison’s own logic. For a self-funded buyer acquiring a founder-led business, the governance question is identical in kind if not in scale. How much do you change, and how quickly? Arnault’s answer is: very little, and very slowly. The business worked before you arrived. Your job in the first year is to understand why, not to prove that you know better.

3. Leadership Continuity: The Transition That Did Not Break Anything

The most immediate governance decision any acquirer faces is what to do about leadership. In most acquisitions, this is where the damage begins. The buyer brings in their own people. The institutional knowledge walks out the door with the departing management team. The employees who stayed begin updating their CVs.

Arnault’s approach to leadership transitions is one of the most consistent and deliberate aspects of his model, and the BVLGARI integration illustrates it precisely.

Paolo and Nicola Bulgari remained Chairman and Vice Chairman of the BVLGARI board following the acquisition. Their continued presence was not ceremonial. It was a deliberate signal to everyone inside and outside the business that the brand’s heritage was being protected, not overwritten.

Francesco Trapani, who had run BVLGARI for 27 years and orchestrated its transformation from a €25 million jewellery company into a €1.5 billion global luxury group, did not step aside. He was elevated. Trapani joined LVMH’s Executive Committee and took over the management of the enlarged LVMH Watches and Jewellery division, overseeing not just BVLGARI but Tag Heuer, Chaumet, Zenith, Hublot, Fred, and De Beers alongside it. The man who built BVLGARI was given responsibility for everything Arnault was building in that category.

This arrangement served multiple purposes simultaneously. It gave Trapani a platform that matched his ambition and his track record, removing any incentive he might have had to leave and build elsewhere. It gave LVMH the operational expertise of someone who had spent nearly three decades building relationships with suppliers, craftspeople, retailers, and customers across the jewellery industry. And it gave the BVLGARI brand and its employees the continuity of seeing a familiar face at the helm during the most uncertain phase of any acquisition.

Trapani led the LVMH Watches and Jewellery division until 2014. Three years of controlled transition. By the time he departed, BVLGARI was no longer a newly acquired asset being carefully managed. It was the centrepiece and template of LVMH’s jewellery strategy going forward.

The ETA parallel: My MBA research identified seller continuity as one of the most consistent cross-theme findings across all eleven interviews with acquisition entrepreneurs. One participant described it plainly: “The seller actually stayed on as my employee. It was easier to get that documentation out of his head.” Another sought sellers willing to stay for one to two years specifically to surface undocumented knowledge embedded in customer relationships, team dynamics, and informal processes. Where sellers departed abruptly, whether due to health, emotional detachment, or poorly structured handovers, operational gaps emerged that took months to close. The research also identified operator fit as a critical determinant of governance success, encompassing not just technical skills but cultural alignment, leadership readiness, and motivational congruence. Trapani’s elevation rather than replacement is a masterclass in all three. Arnault did not install a stranger. He retained and empowered the person who already understood every dimension of what he had just acquired.

4. Financial and Strategic Integration: Where the Premium Gets Earned Back

The financial case for the BVLGARI acquisition was built on a specific thesis. BVLGARI had the brand. LVMH had the platform. Together they could do things neither could do alone.

The combination promised synergies in purchasing and distribution, expanded retail presence particularly in Asia, and access to LVMH’s global infrastructure across more than 5,000 stores in 80 countries. Trapani himself said at the time that the entrance into LVMH would allow BVLGARI to reinforce its worldwide growth and to realise noteworthy synergies, in particular in the areas of purchasing and distribution.

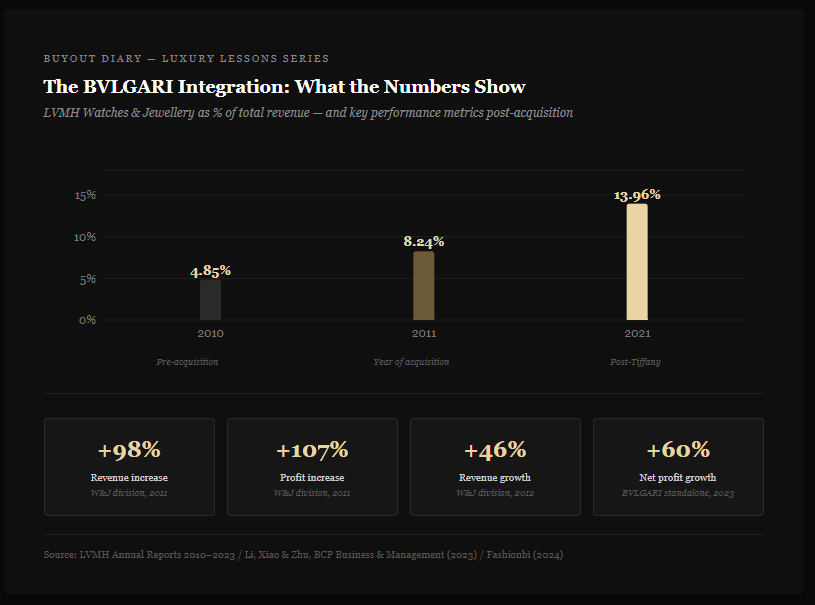

The financial results of the first years confirmed the thesis. In 2011 alone, the Watches and Jewellery division recorded a 98% revenue increase and a 107% profit increase, all attributed to the BVLGARI consolidation. The division’s share of LVMH’s total gross revenue jumped from 4.85% in 2010 to 8.24% in 2011. In 2012, the division continued with a 46% revenue increase and a 26% profit increase, exceeding every other LVMH business group in growth rate.

But the most significant financial decision Arnault made post-acquisition was not about extracting synergies. It was about reinvesting in the brand’s physical infrastructure at a pace the Bulgari family could never have managed independently.

LVMH committed significant capital to opening new BVLGARI flagship stores in the highest-value retail locations globally, with particularly strong expansion in Asia, a market where the brand had significant recognition but limited physical presence. In 2017 alone, BVLGARI achieved excellent performance and continued to gain market share thanks to the strength of its iconic lines Serpenti, B.Zero1, Diva, and Octo, with growth particularly strong in Asia, the United States, and Europe.

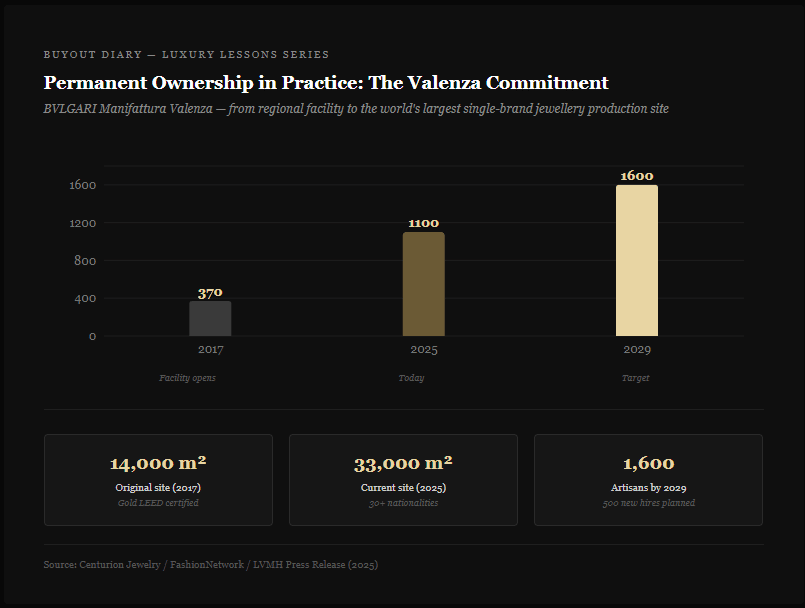

The most visible long-term capital commitment was the Valenza manufacturing facility. In 2017, LVMH opened what was then Europe’s largest jewellery manufacturing site for BVLGARI in Valenza, Italy, the heart of the country’s goldsmithing district, with 370 artisans. By 2025, that facility had grown from 14,000 to 33,000 square metres and now employs 1,100 artisans from more than 30 nationalities. BVLGARI has since expanded it further, declaring it the world’s largest single-brand jewellery manufacturing site, with plans to grow to 1,600 artisans by 2029.

This is not operational efficiency. It is a decades-long capital allocation decision rooted in a conviction that the brand’s manufacturing heritage is a competitive advantage worth protecting and expanding. Arnault reinvested in the thing that made BVLGARI exceptional rather than replacing it with something cheaper and more scalable.

The ETA parallel: Arnault’s capital allocation model has a direct equivalent at the SME level. When you acquire a business, the first question is not how to cut costs. It is which parts of the business are worth reinvesting in because they are genuinely exceptional and defensible. The business owner spent years building those parts. Your job is to identify them and fund them properly, perhaps for the first time. That is where the premium gets earned back. My MBA research found that phased delegation worked best when acquirers began with operational support before gradually transferring full profit and loss responsibility, and that control mechanisms such as dashboards, financial reporting, and strategic check-ins ensured accountability without tipping into micromanagement. The same logic applies to capital: deploy it in phases, anchored to what the business tells you rather than what your model assumes.

5. Cultural Integration: Preserving the Roman Soul

BVLGARI is, in the most precise sense, a Roman brand. Not Italian in the general sense, but specifically Roman. The bold colours, the architectural forms, the references to ancient mythology and classical antiquity: the design language of BVLGARI is inseparable from the city it was born in and the culture it grew out of.

This identity is not marketing. It is the foundation of why the brand commands the prices it charges and attracts the customers it attracts. Dilute it, and you dilute the thing the customer is paying for.

Arnault understood this before he bought the business. The cultural commitments built into the combination agreementwere not afterthoughts. LVMH committed to preserving the Bulgari identity and the values that had made it one of the most attractive names in the luxury sector. The headquarters remained in Rome. The design direction remained distinctly BVLGARI. The brand did not become a generic LVMH house. It remained, and remains today, unmistakably itself.

BVLGARI’s hotel operations present an interesting case study within the broader integration. The Bulgari Hotels and Resorts joint venture with Marriott predated the LVMH acquisition, and the question of how that operation would sit within the LVMH structure required careful handling. The answer was consistent with the broader philosophy: the brand identity was preserved, the properties remained distinctly BVLGARI in their aesthetic and positioning, and LVMH’s resources enabled the expansion of the portfolio rather than the consolidation of it.

LVMH uses brand identity as a governance mechanism in a way that most acquirers never attempt. Rather than imposing holding company standards on acquired businesses, a common approach that tends to flatten the distinctive qualities that made the business worth acquiring in the first place, Arnault uses each brand’s own identity as the standard against which decisions are made. The question is not whether a decision fits the LVMH playbook. It is whether it fits what BVLGARI is.

This approach requires a level of intellectual humility that is genuinely rare in acquirers. It means accepting that the business you bought knows things about itself that you do not yet know. It means resisting the temptation to impose your own frameworks before you have earned the right to do so.

The ETA parallel: The businesses with the deepest succession opportunities across Europe and the UK are the ones most rooted in a specific local identity. A local family-run maintenance business has its own culture: relationships with specific suppliers, a reputation with specific customers, a way of doing things that took decades to build. My MBA research found that one of the most disruptive things a new acquirer can do is implement technology or system changes too quickly, before understanding how the existing infrastructure was serving the business. One participant described a situation where a buyer changed the point-of-sale system, the internet infrastructure, and the operational software in the first weeks, and nothing worked. The business lost continuity it had taken the previous owner years to build. The buyer who arrives with a playbook from another context and applies it immediately will destroy that culture before they understand what it was worth.

6. Results, Lessons, and the Template It Created

BVLGARI’s sales resilience within LVMH has been documented consistently even as the broader luxury market has faced pressure. In fiscal year 2023, Bulgari Gioielli S.p.A. recorded a net profit increase of over 60%, with revenue growth of approximately 22% and operating income growth of over 53%, outperforming the overall personal luxury goods market which grew at a more modest 4 to 5% during the same period. In LVMH’s 2025 results, BVLGARI was cited among the brands demonstrating resilience even as the group’s overall Watches and Jewellery segment faced headwinds.

From a €890.5 million revenue business struggling with post-recession cash flow in 2010 to a brand generating revenues that have grown multiples beyond that figure, the compounding effect of patient, well-structured integration over more than a decade is visible in the numbers.

BVLGARI became the template for LVMH’s later jewellery acquisitions, most notably the 2021 acquisition of Tiffany & Co. for $15.8 billion, the largest deal in LVMH’s history. The governance model, the leadership transition approach, the cultural preservation philosophy, and the capital reinvestment strategy developed through the BVLGARI integration were all applied again, at significantly greater scale, when LVMH absorbed the American institution.

LVMH Watch Week, the group’s annual gathering of its watches and jewellery maisons, now features BVLGARI as a centrepiece brand, demonstrating how fully it has been woven into the LVMH ecosystem without losing its individual identity. The brand attends alongside TAG Heuer, Hublot, Zenith, and the others as an equal participant, not a subordinate one.

Three lessons that apply at every deal size:

Governance must fit the business, not the spreadsheet. LVMH’s federated model works because it starts from what each brand is rather than what the holding company needs. My MBA research found that the most effective acquirers design governance structures adaptively, blending informal trust with lightweight formal mechanisms, rather than applying a fixed template regardless of the business’s maturity or cultural context. If your governance structure requires the business to become something different in order to perform, you have the wrong structure.

Delegate with frameworks, not with rules. BVLGARI’s management team was trusted to run the brand according to its own values and logic, supported by LVMH’s resources and held accountable for results. That is not the same as giving them free rein. It is giving them clear accountability with the tools to meet it. The research found that delegation maturity increased in line with the confidence, systems, and trust established following the acquisition. It is a process, not a handover.

Balance legacy and performance. The tension between preserving what made a business worth acquiring and pushing it to perform at a higher level is permanent. Arnault does not resolve that tension. He manages it continuously. The 127-year-old Roman jeweller now operates out of the world’s largest single-brand jewellery manufacturing facility. Both things are true simultaneously.

Coming Up in the Series

Next in the Luxury Lessons series: Tiffany & Co.

A different deal entirely. Bigger, more complicated, and involving a negotiation that broke down publicly, went to court, and was eventually resolved at a renegotiated price nine years after BVLGARI and with a very different set of conditions.

Everything Arnault learned from BVLGARI he applied to Tiffany. And everything that made Tiffany harder is worth understanding if you want to know what the limits of his model look like.

That issue will appear in Buyout Diary in the coming weeks.

One last thing before you go.

The BVLGARI integration worked because Arnault had thought carefully about every one of these dimensions before the ink dried. Most buyers have not. If you are in the middle of a search, have recently acquired, or are an investor thinking about what good post-acquisition governance looks like in the European market, I would genuinely like to hear from you.

Hit reply and tell me: what is the hardest part of the post-acquisition phase that nobody talks about honestly?

I read every reply.

See you next Monday.

Alexander